Insurance Claims Red Flags: How Claims Teams Find Issues Buried in Long Files

Insurance claims red flags are rarely obvious.

In complex claims, the details that matter most are often buried in long files filled with medical records, adjuster notes, claim forms, emails, employer documents, policy language, bills, attachments, handwritten notes, and scanned PDFs. A single claim file can run hundreds or even thousands of pages. In that environment, the biggest review risks are not always dramatic signs of fraud. More often, they are small inconsistencies, missing details, duplicate medical records, or pieces of context that appear once and then disappear into the file.

That is exactly why red flags get missed.

Claims teams are under constant pressure to move quickly. Adjusters, examiners, nurse reviewers, SIU teams, and managers do not have unlimited time to read every page closely, compare every statement across every document, and manually trace every inconsistency back to its source. As a result, only a small number of claims receive the kind of deep red-flag review that would actually surface the most important issues.

Brad Schneider, CEO of Nomad Data, puts the challenge plainly:

“Finding insurance red flags in long, unstructured text documents is not something that people do well. It also requires an incredible amount of time to do thoroughly, and that’s typically time that insurance companies don’t have.”

That creates a gap between what claims teams know they should check and what is practical to check at scale. It also creates real downstream consequences: slower investigations, inconsistent handling, more leakage, more fraud exposure, and missed opportunities to follow up on issues that could materially change the outcome of a claim.

The problem is not a lack of expertise. The problem is that modern claim files are too large, too fragmented, and too unstructured for manual review alone to catch everything that matters.

What counts as an insurance claims red flag?

Insurance claims red flags are details in a claim file that may warrant follow-up, clarification, escalation, or deeper review.

That definition matters because red flags are often treated too narrowly. They are not limited to obvious fraud indicators. In practice, an insurance claims red flag can point to many different types of claim issues, including documentation gaps, medical uncertainty, claim complexity, coverage questions, exclusion issues, inconsistencies between records, duplicate medical records, or possible fraud.

In other words, a red flag is not automatically proof of wrongdoing. It is a signal that something deserves attention.

For claims teams, that broader definition is more useful. The goal is not simply to “catch fraud.” The goal is to identify the details that may change how a claim should be handled, what questions should be asked next, whether additional documentation is needed, or whether the claim should be escalated for deeper insurance claims investigation.

That distinction matters in day-to-day claims operations because many valuable red flags are operational, medical, or procedural before they become investigatory.

A missing document may delay resolution. A date inconsistency may affect causation. A prior injury may change the interpretation of a medical record. A policy exclusion may change the handling path. A duplicated record may create confusion around the true evidence in the file.

The value of red-flag review is not limited to identifying suspicious behavior. It is about giving claims professionals better visibility into the file so they can make faster, more consistent, and more defensible decisions.

Non-fraud red flags claims teams should catch first

The first and most important category of insurance claims red flags includes issues that may materially affect handling even when fraud is not the primary concern.

These are the red flags that often show up in ordinary claim files: inconsistent timelines, missing documentation, conflicting medical information, unclear work status, or buried references that change the context of the claim.

They may not be dramatic, but they matter.

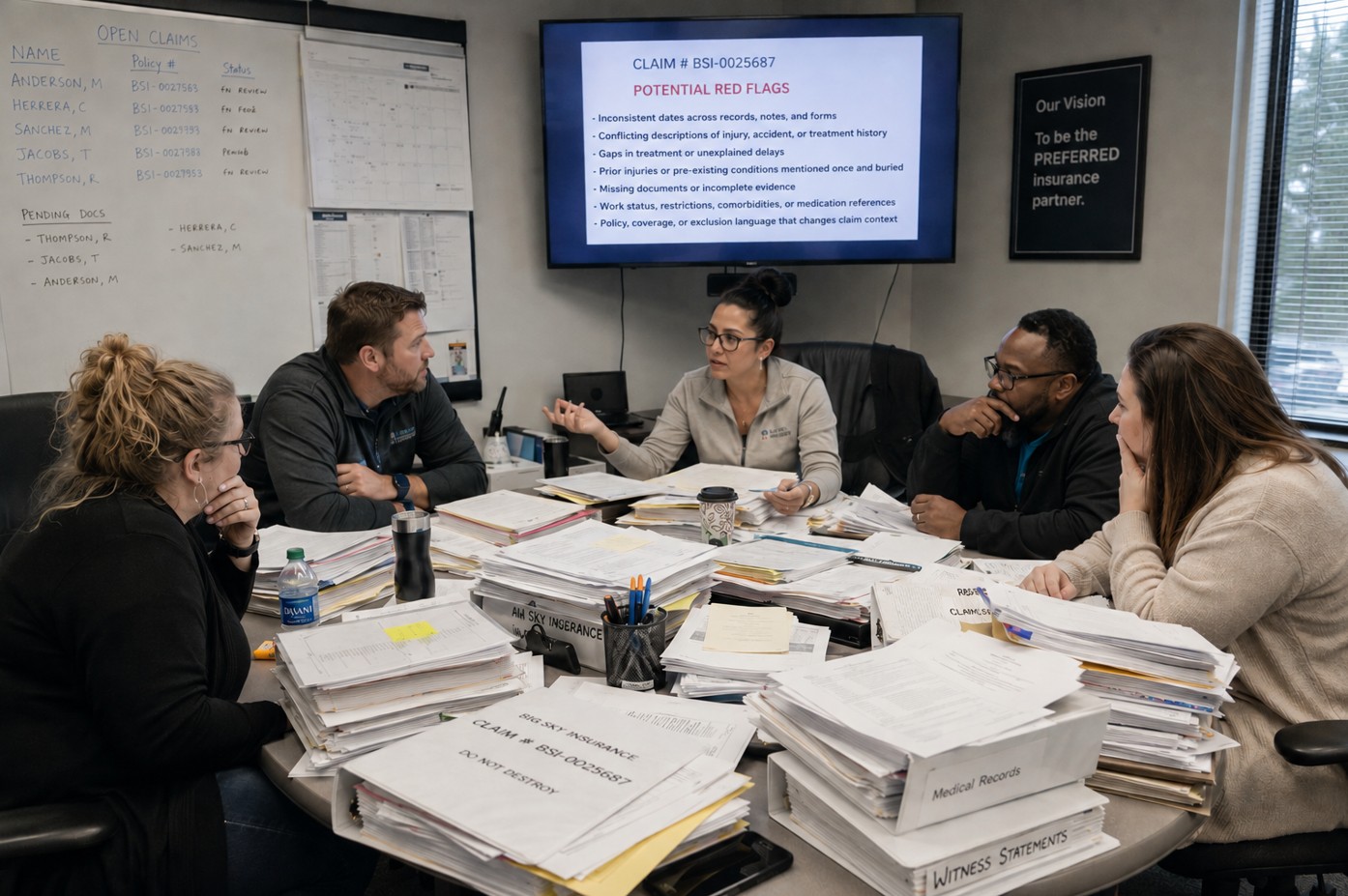

Inconsistent dates across records, notes, and forms

Dates are one of the most common sources of buried inconsistency in a claim file.

The date of injury, date of first treatment, incident reporting date, work status change, return-to-work date, surgery date, or date of maximum medical improvement may differ across forms, physician notes, employer records, adjuster documentation, bills, and correspondence.

A single mismatch may be explainable. But it may also affect causation, claim timing, notice requirements, benefit calculations, or the sequence of events the file is supposed to support.

In a long file, small date inconsistencies are easy to miss because each document can look reasonable in isolation. One form says the injury happened on a Tuesday. A provider note references symptoms beginning a week earlier. An employer document shows a different reporting timeline. An adjuster note introduces another version.

None of these details may seem significant on their own. But when viewed together, they may create a question that needs to be resolved.

The challenge is that manual review requires the reviewer to find each date, remember it, compare it, and understand whether it conflicts with the rest of the file. That is difficult in a 50-page file. It becomes much harder in a 1,000-page file.

Conflicting descriptions of injury, accident, or treatment history

As claims evolve, incidents get retold. That is normal.

But it also creates risk.

A claimant’s first description of an injury may differ from what later appears in a provider note, a recorded statement, an employer form, or a legal filing. The differences may be subtle: where the incident occurred, what body part was involved, when symptoms began, how severe the initial condition was, or what the claimant reported being able to do after the event.

Brad Schneider highlighted this as one of the clearest examples of why manual review breaks down in long files:

“Many times, you can put together a timeline of how the patient’s narrative has changed, and it can oftentimes lead to inconsistencies in the claim, which begs questions that the examiner can then follow up on.”

That is exactly the point. The value is not only in finding a contradiction. It is in surfacing a specific issue that a human examiner can investigate further.

For example, a medical note may describe pain beginning immediately after an accident, while a later record suggests symptoms started days earlier. A claimant statement may emphasize one injured body part, while later treatment records focus on another. A prior history section may introduce context that does not appear in the initial claim description.

These are not automatic signs of fraud. But they are important insurance claims red flags because they help claims teams understand whether the claim narrative is consistent, complete, and properly supported.

Gaps in treatment or unexplained delays

A gap in treatment does not automatically mean anything improper happened. But it often changes claim context.

A long delay before treatment begins, a sudden break in care, an unexplained pause between visits, or an abrupt escalation after a quiet period may raise questions about severity, causation, recovery, or continuity of symptoms.

In complex files, these treatment gaps may only become visible when someone pieces together records across multiple providers and time periods. That is difficult to do manually, especially when the records are not chronological and the timeline has to be reconstructed from fragmented evidence.

For example, one provider’s records may end in March, another may begin in July, and a separate bill may reference treatment that is not included in the file. A quick review may miss the gap entirely.

These gaps matter because claims teams often need to understand not only what happened, but when it happened and whether the supporting documentation aligns with the claim.

Prior injuries or pre-existing conditions mentioned once and buried

This is one of the most important red flags in injury-related claims.

Brad pointed to the classic example:

“If you’re receiving thousands and thousands of pages of medical records, and there happens to be a needle in a haystack where perhaps a knee injury was reported before an accident, it can be extremely hard to find that manually.”

Pre-existing conditions are rarely surfaced neatly for the reviewer. They may appear in one intake note, one physician history section, one prior imaging report, one medication list, or one passing reference deep in the medical record.

If that reference is missed, the claim may be evaluated without critical context.

This is not a niche problem. It is one of the clearest examples of why long-file review creates operational risk even when no one is trying to deceive anyone. The relevant fact may simply be buried.

Prior injuries, chronic conditions, previous surgeries, related complaints, recurring pain, comorbidities, or earlier treatment history can all affect how a claim is understood. The issue is not that every prior condition changes the outcome. The issue is that claims teams need to know the context exists so they can evaluate it appropriately.

Missing documents or incomplete evidence

Claims teams also need to catch what is not in the file.

Missing records, absent employer documentation, incomplete medical histories, unsigned forms, missing bills, incomplete police reports, missing policy documents, or missing correspondence can all slow claim resolution or distort claim review.

In long files, it is surprisingly easy to assume something is present because the file feels complete.

But volume is not the same as completeness.

A claim can contain thousands of pages and still be missing one document that matters. It may have multiple medical records but no complete treatment history. It may include bills but not the underlying clinical notes. It may include policy excerpts but not the full policy language. It may include adjuster notes that refer to attachments that are not actually present.

These are important insurance claims red flags because they help teams avoid false confidence. The question is not just, “What does the file say?” It is also, “What should be here that is missing?”

Work status, restrictions, comorbidities, or medication references

Important claim context often appears in isolated references rather than in summary form.

A provider may mention work restrictions in one progress note. Another note may refer to a comorbidity that affects recovery. Elsewhere, medication references may suggest severity, prior treatment, or unrelated medical history that changes the interpretation of the claim.

These are not always headline issues. But they are often exactly the kinds of details that adjusters, examiners, nurse reviewers, or managers would want surfaced during review.

For example, one note may say the claimant is cleared for light duty. Another may indicate restrictions that conflict with the employer’s return-to-work record. A separate record may mention a condition that affects recovery time. A medication reference may suggest treatment history that is not otherwise obvious.

When these details are buried across a large file, claims teams may miss them unless they are specifically looking for each category.

Policy, coverage, or exclusion language that changes claim context

Some of the most important red flags are not medical at all.

A policy condition, exclusion, limitation, definition, endorsement, or notice requirement may materially affect how a claim should be reviewed. In long files, policy language is often separated from the facts of the claim, making it harder to connect the rule to the underlying evidence.

That means red-flag review must include both the claim documents and the governing policy material. Otherwise, the reviewer may identify facts without understanding how they matter.

For example, a fact pattern may appear ordinary until it is compared against a specific exclusion. A timing issue may matter only because of a policy condition. A loss detail may be significant only because of how the policy defines the covered event.

This is where claims review becomes more than document summarization. The system needs to help connect facts, dates, records, and policy language so human reviewers can decide what matters.

Claimant statements that do not match medical or employer records

Another common red flag is misalignment across sources.

A claimant statement may not fully match employer records, physician notes, adjuster correspondence, witness statements, or other file materials. Sometimes the difference is minor. Sometimes it is the kind of inconsistency that requires a follow-up question before the claim can be handled confidently.

Again, the operational value is not just in noticing that two statements differ. It is in finding those differences consistently across many claims, not just the few files that receive unusually deep manual review.

A claim may contain several versions of the same event across different documents. Human reviewers are very good at evaluating those inconsistencies when they see them. The hard part is making sure the right inconsistencies are actually surfaced.

Fraud-related red flags that may require insurance claims investigation

Not every red flag points to fraud. But some patterns do justify deeper insurance claims investigation, especially when several issues appear together.

This is where careful framing matters. A red flag is not proof. It is a reason to look closer.

For SIU teams, claims managers, and examiners, the goal is to identify which files deserve additional scrutiny, what issues should be reviewed, and where the supporting evidence appears in the file.

Duplicate medical records or duplicate language across documents

Duplicate medical records are a strong example.

A file may include repeated records, duplicated pages, repeated bills, copied narrative sections, or near-identical language across documents that should not read the same way. Sometimes duplication is administrative. Sometimes it may be harmless file clutter. But in other cases, it may warrant deeper investigation.

This is one reason duplicate medical records is such an important signal. On its own, duplication may not prove much. In context, it may be one of several indicators that the file deserves closer scrutiny.

Duplicate medical records can also create practical problems even when there is no fraud concern. They can inflate file size, slow review, confuse timelines, create uncertainty around what is original versus repeated, and make it harder to identify the most relevant evidence.

A claims team reviewing a long file needs to know whether a document is unique, repeated, revised, or inconsistent with another version. That is difficult to determine manually when records are scanned, repeated, or embedded in large PDFs.

Reused phrasing, copied notes, repeated bills, or conflicting versions

Fraud-related concerns often emerge through patterns rather than single events.

A repeated phrase across records, multiple versions of the same document, conflicting medical narratives, or repeated billing items may not stand out during a quick skim. But when grouped together, they may suggest that something is wrong with the file, the documentation, or the claim narrative.

For example, multiple provider notes may contain unusually similar language. Bills may repeat in a way that requires clarification. A document may appear in two versions with small but meaningful differences. A later record may revise or contradict a prior statement.

These are the kinds of issues that can be hard to detect without comparing documents across the full file.

Escalation triggers hidden in adjuster notes or correspondence

Some of the most important investigation signals are not in the formal claim documents at all. They are buried in adjuster notes, internal comments, emails, or correspondence.

That matters because manual reviewers often focus first on the obvious documents: forms, records, and medical material. But escalation clues may sit elsewhere in the file, disconnected from the supporting evidence that would make them meaningful.

An adjuster note may mention a concern that was never fully resolved. A piece of correspondence may reference a missing document. An internal comment may flag a timeline issue. An email may mention a potential inconsistency that never makes it into the formal summary.

These hidden signals can be important insurance claims red flags because they show what the team already suspected, questioned, or needed to clarify.

Patterns become more concerning when multiple red flags appear together

This is where insurance claims investigation becomes much more effective.

A duplicate record alone may not mean much. A timing inconsistency alone may not mean much. A changed narrative alone may not mean much. But when duplicate medical records, conflicting injury descriptions, unexplained treatment gaps, and a buried prior condition all appear in the same claim, the total pattern becomes more significant.

That is exactly the kind of combined signal that is difficult to detect manually across long files and exactly the kind of pattern AI can help surface systematically.

The goal is not to replace human judgment. It is to make sure the human reviewer sees the full pattern before deciding what to do next.

Why manual red-flag review is so difficult

The manual challenge is not just reading speed. It is cognitive overload.

As Brad Schneider explained:

“People are just not good at remembering lots of facts and holding them all in their head at once.”

That is the core issue. A reviewer may notice an important detail on page 87, another on page 412, and a third in an email attachment near the end of the file. The problem is not noticing one fact. The problem is holding all of them together long enough to compare them accurately.

In large claim files, that is extremely difficult.

To do it thoroughly would take an enormous amount of time, and most insurers simply do not have that time. The cost is prohibitive. The volume is too high. The workflow pressure is too constant. As a result, only a small subset of claims get the scrutiny required to uncover many of these red flags.

That means organizations often check only a handful of known signals, in a limited number of files, under tight time pressure. The review is necessarily selective.

The result is inconsistent outcomes. Some important issues are found. Many are not.

Manual review also becomes harder because claims files are rarely clean. Records may arrive out of order. Scanned pages may be low quality. Attachments may be duplicated. Handwritten notes may be difficult to read. Tables, forms, bills, and medical records may all use different formats. Important context may be spread across documents that were never designed to be read together.

This is why claims teams need more than simple search. Searching for one keyword can help find one known issue, but insurance claims red flags are often contextual. A date inconsistency requires comparison. A treatment gap requires a timeline. A duplicate record requires document matching. A coverage question requires connecting facts to policy language.

That is where traditional manual processes break down.

How AI helps claims teams find red flags in long files

This is where AI changes the economics of review.

Nomad Data’s Doc Chat is not just a search tool or a summarizer. It can act as a systematic red-flag review system across long, unstructured claim files. Instead of relying on a human reviewer to remember every possible issue and manually compare every relevant document, Doc Chat can check claims against a large library of red flags across the full file.

Manual review forces selectivity. AI makes comprehensive checking possible.

With Doc Chat, claims teams can:

- Run large sets of red flags against every claim

- Search across the entire file, not just one document at a time

- Compare records and narratives across sources

- Identify duplicate medical records

- Surface inconsistencies by category

- Find missing or incomplete evidence

- Connect claim facts to policy language

- Suggest additional red flags

- Support faster escalation and follow-up

- Provide source-backed answers that reviewers can verify

Just as importantly, this can be tailored to the insurer’s own business.

That point matters because skepticism around AI is often driven by experience with generic consumer tools. Many people have seen AI struggle with messy PDFs, large documents, tables, forms, scanned images, or handwriting. But enterprise claims review requires more than a general-purpose chatbot.

Nomad Data’s approach is different. Doc Chat is configured around the insurer’s own rules, products, workflows, and red flags. The goal is not for insurers to trust Nomad Data as the subject matter expert in every niche line. The goal is to help insurers apply their own best practices systematically and at scale.

Brad described this as a core advantage of using AI in long-file review:

“The value is not that AI replaces the claims professional. The value is that it can apply a consistent review process across files that are far too long and complex for people to review the same way every time.”

That is especially valuable in complex lines of business, large files, or high-volume environments where manual consistency breaks down.

Why citations matter in claims review

Claims teams do not need AI to make the final decision for them.

They need AI to help them find what matters and prove where it came from.

That is why citations matter so much in claims review. A black-box answer is not enough. If an AI system says there is an inconsistency, a duplicate record, a missing document, or a possible pre-existing condition, the reviewer still needs to verify it before acting.

Brad described the value clearly:

“Citations remove the burden of trust on the AI.”

Instead of asking the user to simply accept a conclusion, Doc Chat can show the source material behind it. The human reviewer can then draw their own conclusions based on the exact document and page.

This is powerful for two reasons.

First, it supports better decisions. Claims teams can validate findings quickly and confidently.

Second, it supports adoption. Human trust in AI is still developing, especially in high-stakes workflows like claims handling and insurance claims investigation. Source-backed answers make AI easier to use because they fit the way experienced professionals already work: review, verify, decide.

In that sense, citations are not a nice-to-have feature. They are essential to making AI usable in claims workflows where reviewers need to verify every finding.

A claims examiner needs to know where a statement appears. A manager needs to understand why a claim was escalated. An SIU team needs to see the underlying evidence. A nurse reviewer needs to verify the medical record. A compliance or legal team may need a clear audit trail.

Source-backed AI answers help support all of those workflows.

Moving from selective review to systematic review

For years, claims teams have known that long files hide important issues. The problem was that fully checking for them at scale was too expensive and too time-consuming to be practical.

That is the real change AI makes possible.

Instead of asking a reviewer to manually remember every potential issue, claims teams can configure a repeatable red-flag review process. Instead of checking only a small subset of claims, they can apply more consistent scrutiny across a broader claim inventory. Instead of relying on a handful of keyword searches, they can look for patterns across dates, documents, narratives, medical records, bills, policy language, and correspondence.

This changes how claims teams approach long-file review.

Claims teams can move from reactive review to proactive review. They can move from selective red-flag checks to systematic red-flag detection. They can give human reviewers a better starting point, with the most relevant issues surfaced and cited before deeper review begins.

That does not mean every claim becomes an investigation. It means teams are better equipped to identify which claims need attention and why.

Faster review, better human judgment

AI should not decide whether a claim is valid, payable, or fraudulent.

Human claims professionals still need to make those decisions.

What AI can do is make sure fewer important details stay buried in long files. It can help claims teams review more consistently, investigate more effectively, reduce leakage, identify duplicate medical records, save time, and apply scrutiny across many more claims than manual workflows allow.

That is the real opportunity behind insurance claims red flags.

Claims organizations do not need generic AI layered on top of complex workflows. They need systems built for the way claims work: long files, messy documents, sensitive decisions, source-backed answers, and human review.

With Nomad Data’s Doc Chat, claims teams can use AI to review large files, surface red flags, support faster insurance claims investigation, and give examiners the context they need to make better decisions.

As Brad Schneider put it:

“The goal is to help claims teams find the issues they would want to find if they had unlimited time. AI makes that kind of review possible at a much larger scale.”

See how Doc Chat helps claims teams find red flags faster

Nomad Data’s Doc Chat helps claims teams review long files, find insurance claims red flags, identify duplicate medical records, and support faster insurance claims investigation with source-backed AI answers.

Instead of forcing claims professionals to manually search through hundreds or thousands of pages, Doc Chat helps surface the dates, discrepancies, missing documents, prior conditions, duplicate records, and policy context that may deserve follow-up.

Want to see how Doc Chat works on real insurance claim files? Talk to Nomad Data to learn how claims teams are using source-backed AI to review long files, surface red flags, and move investigations forward faster.